Personal finance, on a calendar.

Method, concepts, tutorials, and habits for budgeting people who think in days, not categories. Written by the team building CalBudget.

All posts

Budgeting on a Fixed Income: A Calendar Method That Holds Up

Budgeting on a fixed income is a timing problem: one deposit, the same bills, and no slack. A calendar that shows every date makes the same plan hold up month after month.

Single Income Budget: Planning One Paycheck Against Every Bill

A single income budget has no second deposit to absorb a timing mistake. Plan every bill against one paycheck cycle and protect the low week before it arrives.

The 7-Day Budget Reset: Restart a Budget That Stopped Working

A budget reset is not starting over from zero. It is seven short days of rebuilding your budget around real bills, today’s actual balance, and dates you can trust.

The Cash Envelope System, Without the Cash

The cash envelope system works because every category has a hard limit and a deadline. You can keep both rules without carrying cash by turning each envelope into planned spending on real dates.

How to Budget Biweekly Pay Without Losing Track of Monthly Bills

Monthly budgets assume monthly income. If you are figuring out how to budget biweekly pay, the fix is to plan by payday window instead of by month.

Debt Snowball vs Avalanche: Pick the One Your Cash Flow Can Keep

The debt snowball vs avalanche debate is usually framed as math versus motivation. The real deciding factor is whether your cash flow can sustain the extra payment on the date it leaves your account.

The 50/30/20 Budget Rule, Put on a Calendar

The 50/30/20 budget rule splits take-home pay into needs, wants, and savings. Percentages have no dates, though, and dates are where budgets fail. Putting each bucket on the calendar is what makes the rule survive a real month.

How to Stop Living Paycheck to Paycheck, One Dated Week at a Time

How to stop living paycheck to paycheck: put paydays and bills on real dates, find the week that always goes wrong, protect the essentials, and raise your lowest projected day a little every month.

3 Paycheck Months: How to Find Yours and Plan the Extra Check

If you are paid biweekly, two 3 paycheck months arrive every year. Here is how to find yours on a calendar and give the extra check one clear job.

How to Avoid Overdraft Fees With a Bill Calendar

Most overdrafts are timing problems, not spending problems. Here is how to avoid overdraft fees by putting every bill and paycheck on a date and watching the lowest projected balance.

How to Use Two Checking Accounts Without Losing Your Forecast

Two checking accounts can separate bills from spending, but the calendar still needs to show one clear cash-flow story.

How to Plan a No-Spend Week on Your Calendar

A no-spend week works best when allowed expenses, food plans, and the saved money all have dates.

How to Build a Monthly Bill Calendar That Actually Works

A monthly bill calendar works when every bill, subscription, paycheck, and planned payment is tied to the date it affects.

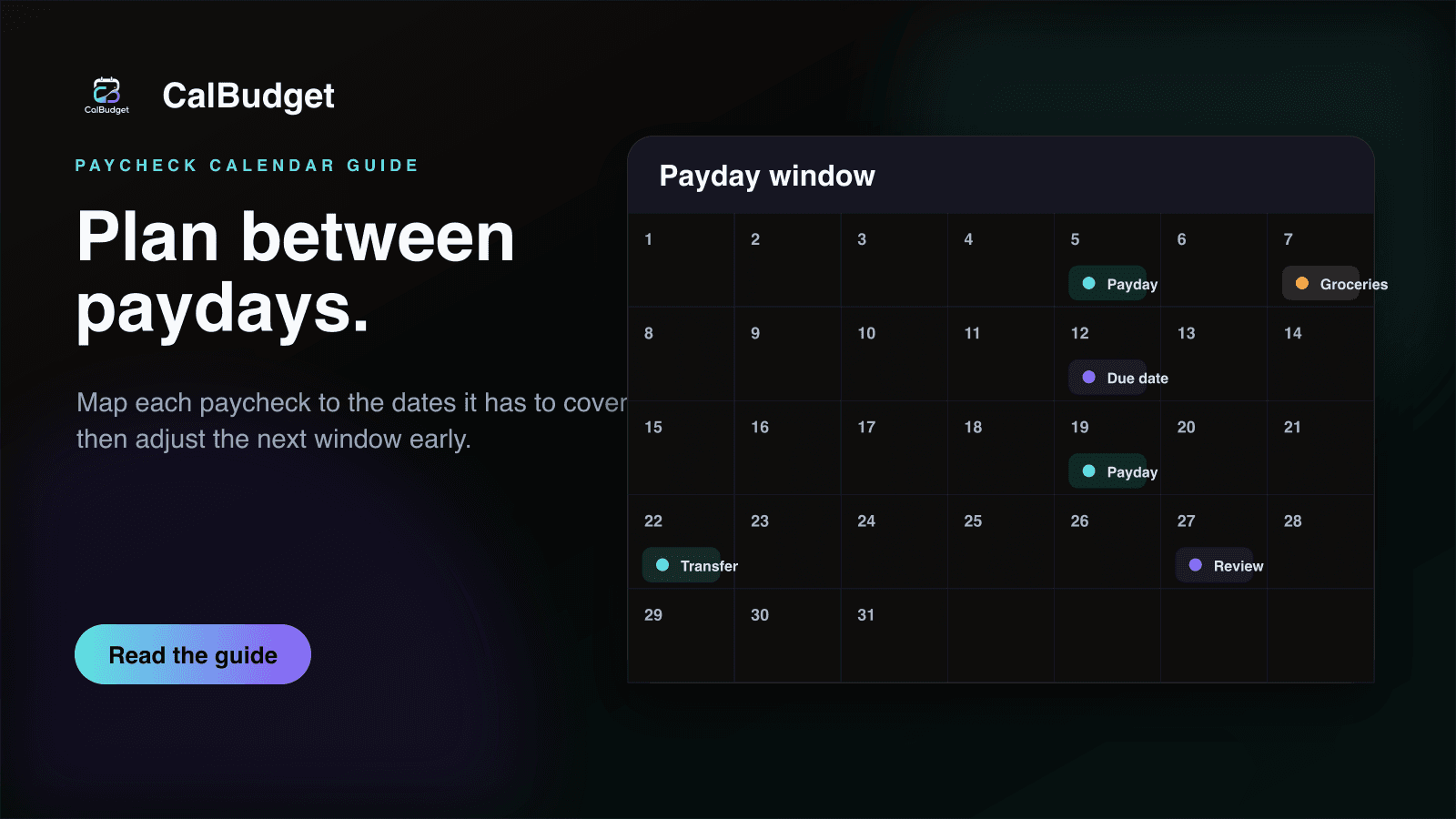

Paycheck Budget Calendar: How to Plan Between Paydays

A paycheck budget calendar helps you plan the dates between deposits instead of hoping a monthly total will work out.

What to Do When Rent Is Due Before Payday

Rent before payday is usually a timing gap, not proof that the whole month is broken.

How to Pay Down a Credit Card With Dated Payments

A card payoff plan works better when the minimum, extra payments, and checking low points share one calendar.

Bill and Expense Trackers: How to Keep Bills, Spending, and Cash Flow Organized

Bill and expense trackers help you see where money is going, when bills are due, and whether your future balance can handle what is coming next.

Turn Annual Bills Into Monthly Calendar Set-Asides

Annual bills stop feeling random when the due date and the monthly set-asides live on the same calendar.

How to Recover After a Large Unexpected Expense

A big surprise bill does not have to break the next three months if the recovery plan starts with dates.

How to Plan Quarterly Taxes on a Budget Calendar

Quarterly taxes are calmer when set-asides, review dates, and payment dates are visible before the deadline.

How to Handle an Irregular Freelance Paycheck Month

Freelance income becomes easier to manage when uneven deposits are matched to the next bills they must cover.

Where Your First $500 Buffer Should Sit

The first $500 of buffer money should protect the lowest day in your forecast, not sit as an abstract savings badge.

Plan Groceries by Payday Window, Not by Month

A grocery budget gets easier when every shopping trip is tied to the payday window it has to survive.

Turn Annual Bills Into Monthly Calendar Transfers

Insurance, memberships, renewals, and taxes stop being surprises when each has a monthly transfer.

How to Run a No-Spend Week Without Guesswork

A no-spend week works better when you choose the week that improves the forecast the most.

Categories Tell You What. Calendar Dates Tell You When.

Both views matter, but cash-flow stress usually comes from when transactions land.

How to Reset Your Budget After a Big Expense

A car repair, medical bill, or emergency purchase does not have to wreck the next three months.

How to Plan for the Paycheck Gap When Starting a New Job

A new job often creates a strange first-month cash-flow gap. Here is how to map it before it surprises you.

Build a Car Maintenance Fund That Actually Gets Used

Oil changes, tires, repairs, registration, and insurance all become easier when they are dated and funded.

The Subscription Rotation Method

Keep the services you actually use by rotating entertainment subscriptions instead of carrying them all year.

Quarterly Taxes Belong on Your Budget Calendar

Freelancers and contractors can reduce tax anxiety by treating estimates as recurring calendar obligations.

Plan Holiday Spending Before December Hits

Gifts, travel, hosting, and annual bills are easier to manage when they appear before the holiday rush.

Budget Calendar vs Spreadsheet: Which One Fits Your Brain?

Spreadsheets are powerful, but calendar budgeting wins when timing is the source of stress.

A Calendar Budget Setup for Couples

How two people can discuss bills, paydays, shared goals, and tight windows without turning it into a spreadsheet meeting.

The Case for Manual Budgeting in a Connected World

Why entering planned transactions yourself can be a feature, especially when you want privacy and intention.

How to Build Your First $500 Cash-Flow Buffer

The smallest useful buffer is the one that protects your lowest projected day, not an abstract savings target.

What to Do When Rent Hits Before Payday

A concrete way to model the first-week squeeze and decide what should move before rent is due.

The Weekly Grocery Budget Is a Calendar Problem

Why grocery planning works better as weekly dated spending than one monthly category cap.

How to Put a Credit Card Payoff Plan on a Calendar

Debt payoff works better when extra payments are scheduled around paychecks and low-balance days.

Budgeting With Two Checking Accounts: A Simple Split

A practical setup for separating bills from spending while still seeing both running balances clearly.

Sinking Funds Make More Sense on a Calendar

Annual bills, car repairs, holiday spending, and insurance premiums are easier to fund when the deadline is visible.

The Bill Due Date Strategy That Smooths Out a Month

How to decide which due dates should move when rent, utilities, cards, and subscriptions all pile into one week.

How to Budget Paycheck to Paycheck Without Guessing

A calendar-first approach for seeing which bills land before each paycheck and which days need attention.

The Quiet Cost of Subscriptions: Auditing Your Recurring Charges

Subscriptions are the slow leak that drains the average household budget. A 30-minute audit, done once a year, typically frees up over $1,000 — without changing your lifestyle.

Variable Income Without the Anxiety: A Freelancer's Guide

Irregular paychecks don't have to mean irregular cash flow. With a smoothing strategy, a tax bucket, and a three-month buffer, freelance income becomes predictable in practice.

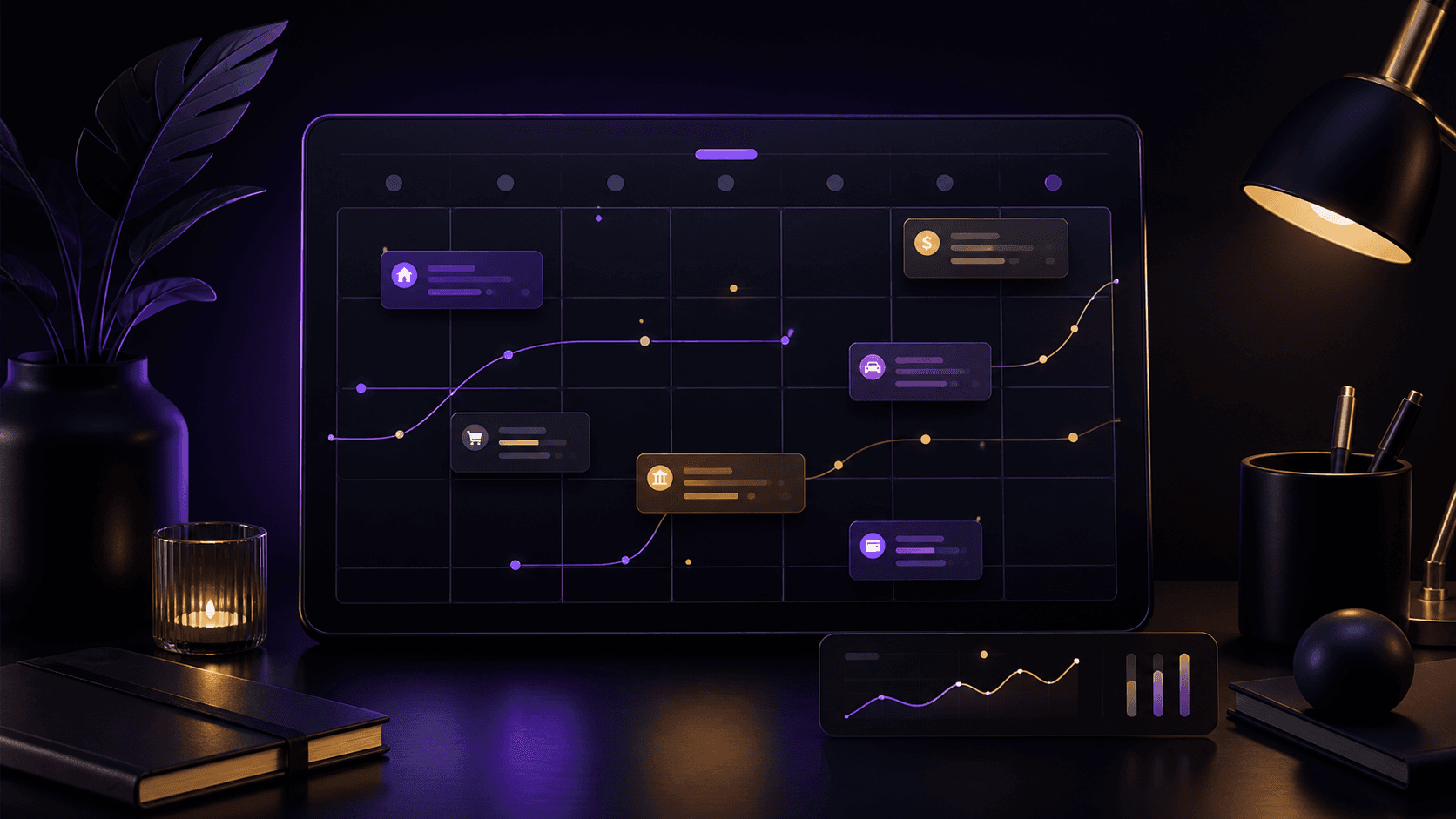

How to Set Up Your First Month in CalBudget (in 15 Minutes)

A blank calendar to a year of forecasted cash flow, in four steps. Account balance, recurring bills, paychecks, ad-hoc spending — in exactly that order.

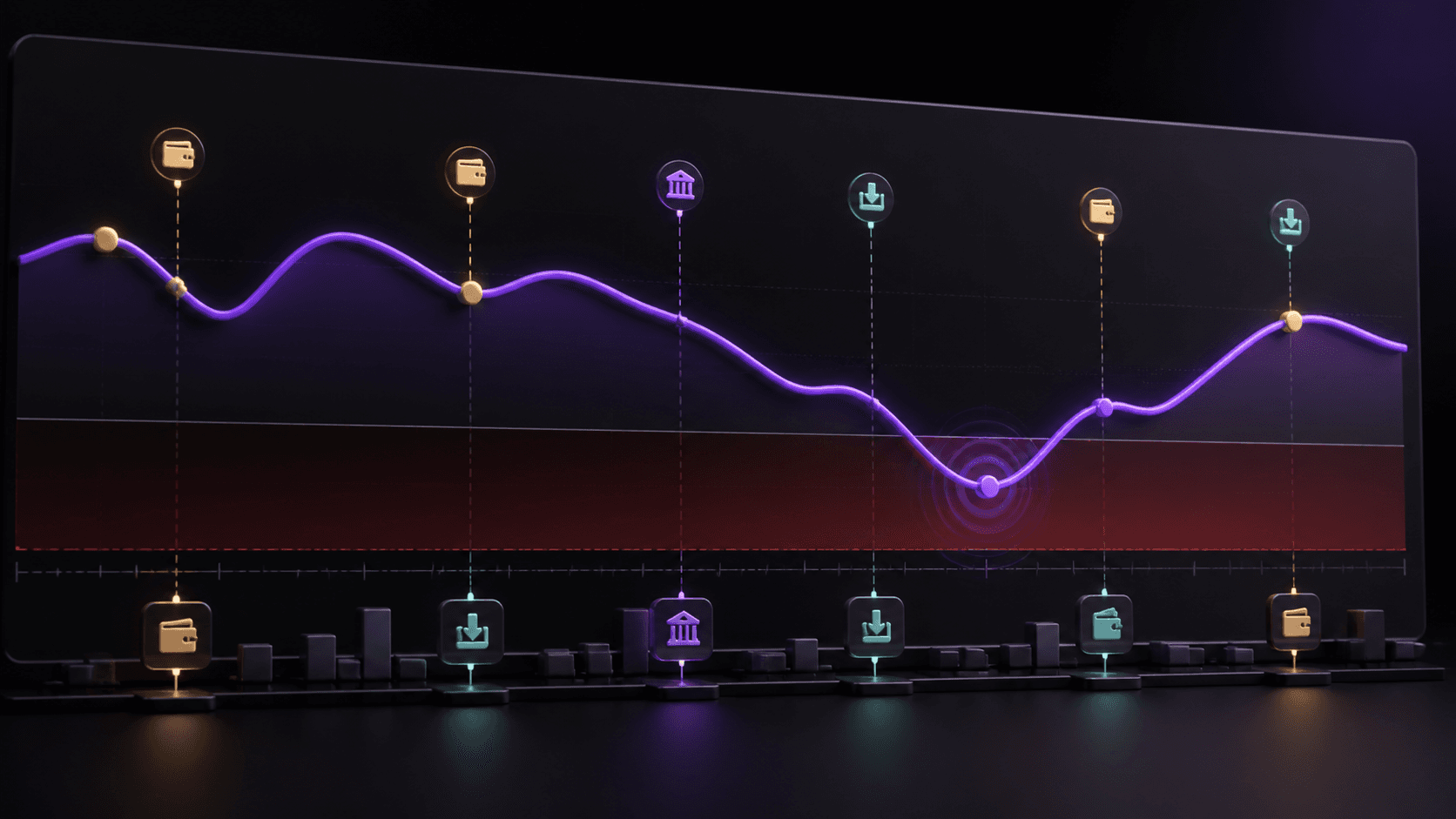

Running Balance: The One Number That Predicts Overdrafts

Most apps show you what your balance is. A running balance shows you what it's going to be — every day, for the next 90 days. That's the entire game.

Why a Calendar Is the Best Budget App You're Not Using

Spreadsheets and transaction lists hide the one variable that matters most: time. A calendar puts your money back on a timeline you can actually plan around.

See your money on a calendar.

Set up your first month in fifteen minutes. Choose Plus for complete planning or Navigator for weekly checkups, action plans, reminders, and shared budget access. Eligible annual subscribers can try either plan for 3 days.

Get started