How to Build a Monthly Bill Calendar That Actually Works

A monthly bill calendar works when every bill, subscription, paycheck, and planned payment is tied to the date it affects.

A monthly bill calendar is useful because bills do not just have amounts. They have dates. Rent on the first, insurance on the twelfth, a card payment on the twenty-first, and a subscription at the end of the month can all be reasonable on their own. The stress starts when several of them land before the next paycheck or when a forgotten recurring charge clears during an already tight week.

That is why a bill calendar app should do more than remind you that something exists. It should show the shape of the month. When every bill, subscription, paycheck, transfer, and planned purchase sits on a date, you can scan the next two weeks and understand what the month is asking from your account before the transactions post.

If a payment can affect your balance, it belongs on the calendar. If the date is uncertain, place it on the most conservative date and adjust later.

Start with the bills that do not move

The fastest way to build a monthly bill calendar is to start with fixed obligations. Add rent or mortgage, utilities, insurance, phone, internet, car payments, credit card minimums, loans, memberships, and any required transfers. These are the dates that create the bones of the month. You can adjust flexible spending later, but fixed bills should go in first because they define the pressure points.

Do not average these bills into one monthly number while you are building the calendar. A $200 payment on the second of the month feels different from the same payment on the twenty-eighth. The amount matters, but the due date tells you whether the payment collides with other bills or lands after income has cleared.

Add recurring bills and subscriptions as their own calendar items

Recurring charges are easy to miss because they usually feel small. Streaming, cloud storage, fitness apps, software, school accounts, toll passes, delivery memberships, and annual renewals often hide in transaction history until they post again. A recurring bill calendar turns those charges into visible dates. Even if you keep every subscription, the point is to stop being surprised by the timing.

- Use monthly repeats for bills that clear on the same day each month.

- Use weekly or biweekly repeats for routines like groceries, transit, childcare, or allowance transfers.

- Use annual repeats for renewals that are easy to forget until the card is charged.

- Add an end date when the payment is temporary, such as a short installment plan or a trial you plan to cancel.

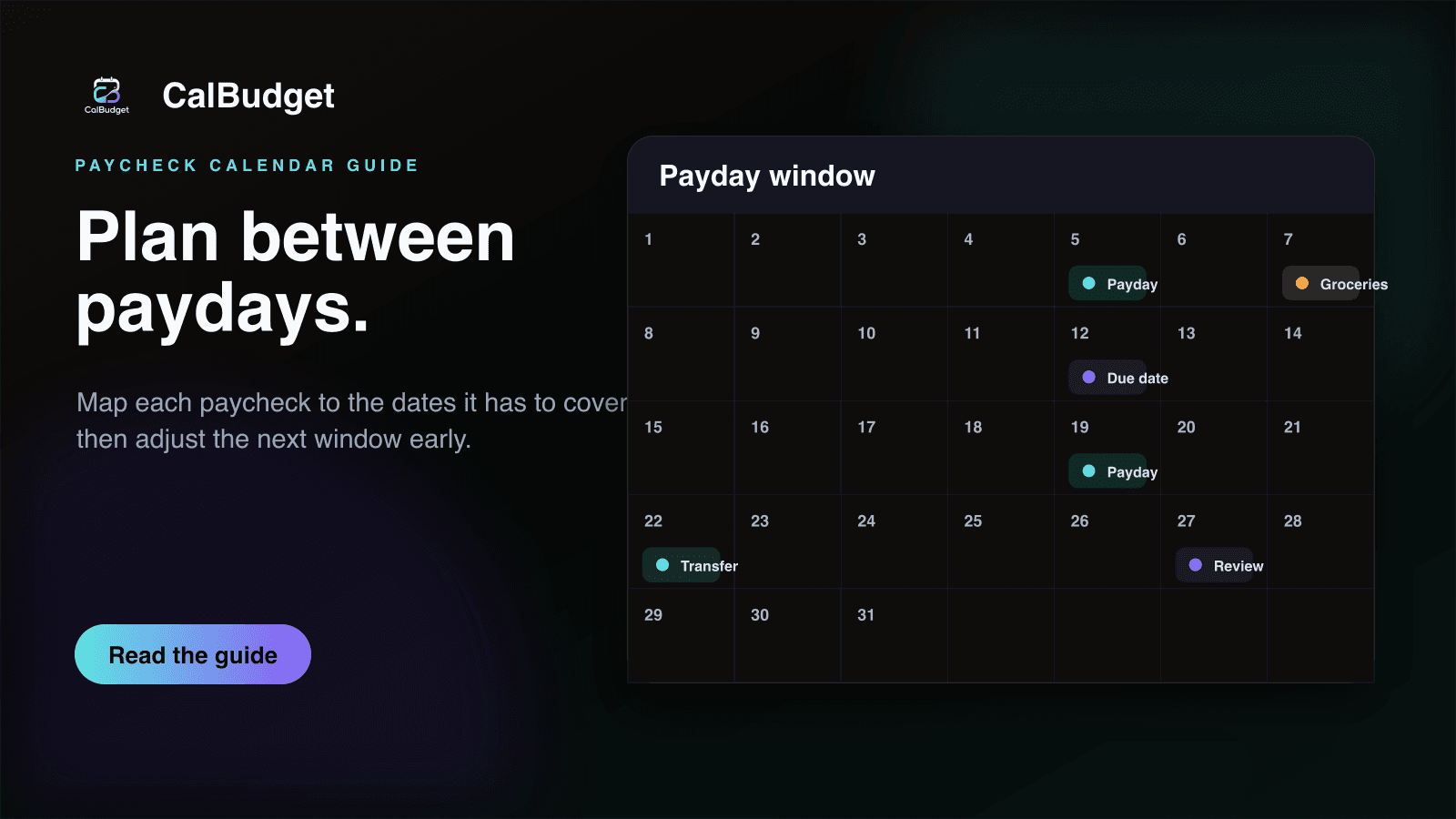

Put paychecks on the same calendar

A bill due date calendar becomes much more useful when income is visible too. The question is rarely whether the whole month has enough money in theory. The real question is whether the bills due before the next paycheck can clear comfortably. Put expected paychecks on their actual dates, then look at the window between one paycheck and the next.

If income is variable, use the date you can reasonably rely on instead of the date you hope for. A conservative paycheck date gives the forecast a little room to be wrong. When money arrives earlier, the calendar gets easier. When it arrives later, the calendar has already been honest.

Look for bill clusters, not just big bills

The hardest weeks are not always caused by one large payment. They often happen because five normal payments stack together. A utility bill, groceries, a subscription, a card payment, and a school cost can create more pressure than one obvious bill because each one looks harmless by itself.

Once your fixed and recurring items are on the calendar, scan each week for clusters. If too many payments land together, decide what can move. Some due dates can be changed with the provider. Some planned purchases can wait a few days. Some subscriptions can be paused or canceled. The calendar does not make the decision for you, but it makes the timing visible enough to choose on purpose.

Move one flexible item and check the forecast again. If the tight week becomes workable, stop there. A bill calendar is most useful when it helps you make one practical change at a time.

Keep categories, but do not let categories hide dates

Categories still matter. Groceries, housing, utilities, subscriptions, debt, transfers, and personal spending all need labels if you want clean reports. But a category total can hide the week that causes the problem. A monthly grocery total may look fine while one grocery trip lands right before rent. A subscriptions category may look small while three renewals clear in the same paycheck window.

The strongest setup uses both: categories for understanding what the money is for, and dates for understanding when the money moves. CalBudget is designed around that combination. You can scan the calendar for timing, then use reports and categories to understand the pattern behind the month.

Review the next 14 days every week

A bill calendar gets better when you review it before the month forces your hand. Once a week, look at the next fourteen days. Confirm bills, update amounts that changed, add anything you forgot, and check the lowest projected balance. This review should be short. The goal is not to rebuild the budget. The goal is to catch one timing problem while it is still small.

- Open the current month and scan the next two weeks.

- Check the next paycheck date and every bill before it.

- Update any estimates with real amounts.

- Move one flexible item if the low point is uncomfortable.

- Add notes for bills that changed so next month starts cleaner.

A bill calendar is not a prettier checklist. It is a timing system for the month you are actually living in.

How Running Balance Predicts Overdraft Risk Before It Happens

After your bills are on dates, use the running balance to understand which day needs attention first.

Frequently asked questions

What is a monthly bill calendar?

A monthly bill calendar is a date-based view of bills, subscriptions, paychecks, transfers, and planned payments so you can see when money is expected to move during the month.

Is a bill calendar better than a bill checklist?

A checklist can show what exists, but a bill calendar shows timing. Timing is what helps you see whether several bills land before the next paycheck.

What should I put on a bill calendar?

Start with fixed bills, subscriptions, debt payments, expected paychecks, transfers, rent or mortgage, utilities, insurance, groceries, and any large planned purchases.

Can I use CalBudget as a bill calendar app?

Yes. CalBudget is built around a calendar view for bills, subscriptions, income, planned spending, recurring transactions, and future running balances.